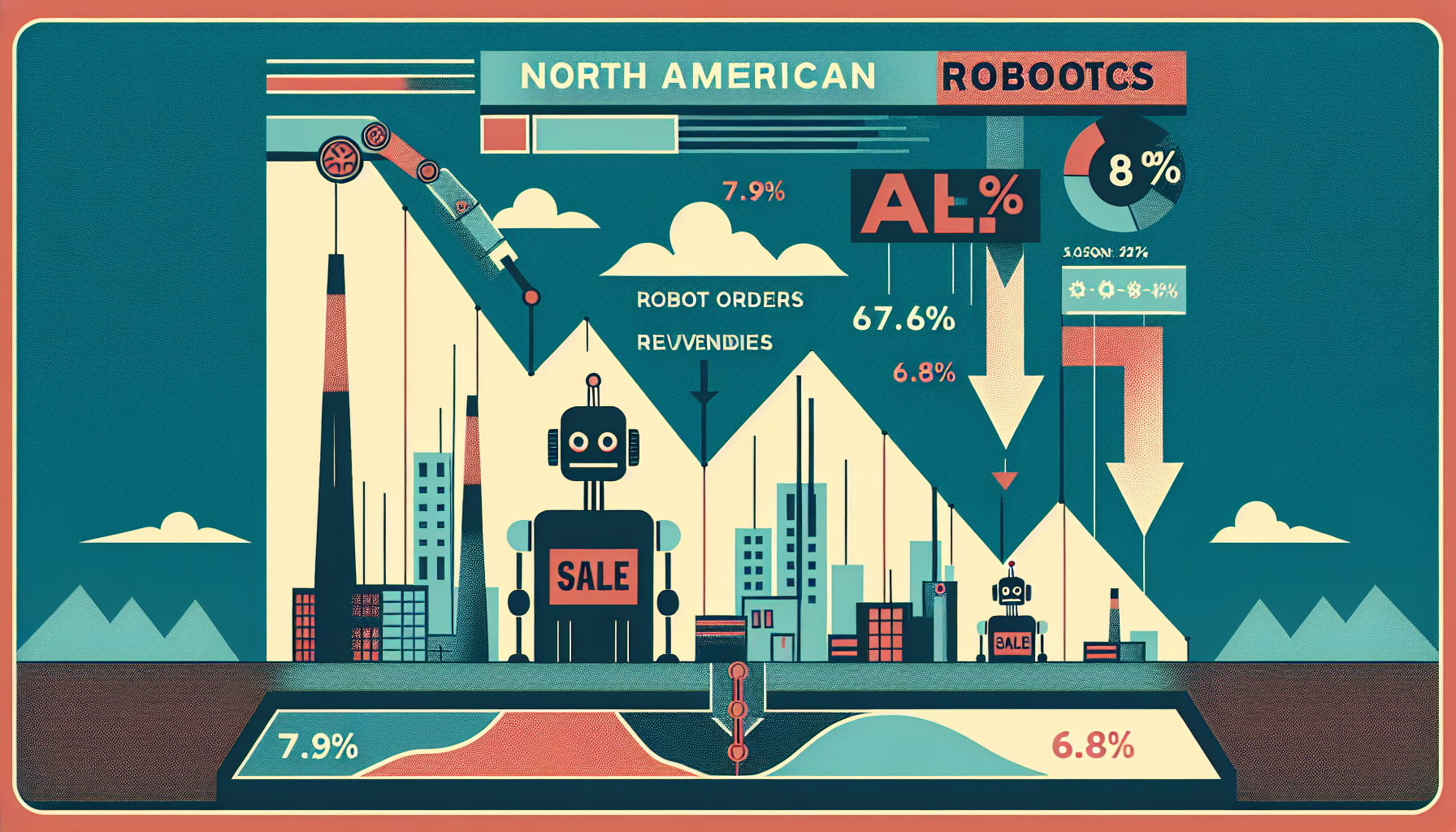

The North American robotics market faced a challenging start in 2024, revealing deeper issues in the economy and manufacturing landscape. As reported by the Association for Advancing Automation (A3), robot orders dipped by 7.9%, and revenues fell by 6.8% in the first half of the year compared to the same period in 2023.

Current Market Landscape

During the first six months of this year, companies in North America placed orders for 15,705 robots, amounting to $982.83 million. This decline is largely due to ongoing economic challenges, such as rising inflation and increased borrowing costs, causing many firms to hold off on significant robotic investments.

Sectors Facing Challenges

Certain industries felt the impact of this downturn more severely than others:

Automotive Sector

The automotive industry presents a mixed picture. Original Equipment Manufacturers (OEMs) in this sector ordered 4,159 robots, marking a 14.4% increase from 2023. However, their revenue fell by 12.0%, totaling $259.96 million. Meanwhile, the Automotive Components sector witnessed a sharp decline. Orders dropped by 38.8% to just 3,574 units, with revenue decreasing by 27.3% to $191.93 million. These figures indicate that component manufacturers are cutting back on automation due to tighter budgets and uncertain future demand.

Semiconductor & Electronics/Photonics

This sector suffered significantly, with robot orders down by 40.0% to a mere 603 units and revenue plunging by 41.4% to $23.43 million. The global supply chain issues and decreased demand for semiconductors are likely behind this reduction in capital spending.

Plastics & Rubber

In the Plastics and Rubber industry, both orders and revenue experienced a decline, although the impact was less pronounced compared to automotive components and semiconductor sectors.

Encouraging Growth in Non-Automotive Sectors

Amidst the decline, some non-automotive sectors showed promising growth:

Food & Consumer Goods

This sector saw significant growth, with robot orders soaring by 85.6% to 1,173 units. Revenue also increased by 56.2%, reaching $62.84 million. The growth trend is fueled by the need for greater efficiency in food processing and packaging, driven by labor shortages and rising operational costs.

Life Sciences

The Life Sciences sector also experienced notable expansion, with a 47.9% upsurge in robot orders totaling 1,007 units, and a remarkable 86.7% rise in revenue, amounting to $47.29 million. This industry’s demand for robotics is propelled by the need for precision and efficiency in operations.

Economic and Market Influences

The reduction in robot sales is largely attributable to broader economic pressures. Rising inflation and higher borrowing costs have led many businesses to defer substantial robotics investments. Nevertheless, the pursuit of efficiency and the demand to supplement the workforce continue to drive interest in automation across varied industries, especially in sectors grappling with labor shortages and higher production expenses.

Looking Ahead

Despite the current slump, optimism within the industry persists. The year 2023 had already witnessed a 30% decline in robot orders following two record-breaking years in sales. As 2024 began, hopes for recovery were high. Although the early part of the year hasn’t aligned with these expectations, businesses retain a positive outlook for the latter half of the year. The ongoing necessity for automation to alleviate labor gaps and boost production capabilities is anticipated to sustain the robotics market.

In conclusion, while the North American robotics market is contending with economic adversities, pockets of resilience and growth exist across different sectors. As businesses work to uphold their global competitive edge, the importance of automation is ever-increasing.

Leave a Reply